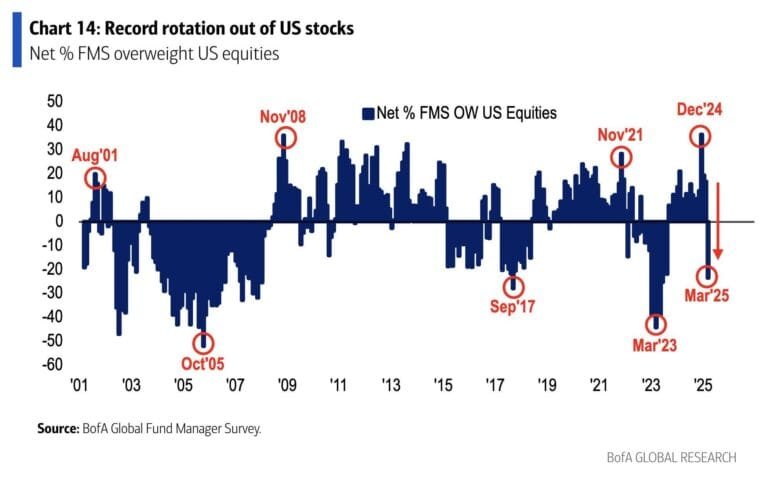

Let's Shape The Future Of Your Investments!

Beat the market with DeepCap's stock picks and investment strategies.

The first week of April 2025 saw global stock markets roiled by an escalating trade war. Over the weekend, the United States enacted a sweeping new round of tariffs on virtually all its trading partners – a move that investors met with a wave of selling. Major equity indices from New York to Tokyo plunged as recession fears mounted, safe-haven assets surged, and governments and companies scrambled to respond to the “tariff shock.” Below we break down the market carnage, the policy reactions from key players, and what may lie ahead in the coming week.

U.S. President Trump’s “reciprocal tariffs” – announced in early April – represent the most dramatic upheaval in trade policy since WWII (Trump tariff global reaction – country by country | Trump tariffs | The Guardian). A blanket 10% import tariff took effect on April 5th, layered on top of steep country-specific duties hitting allies and rivals alike. For example, EU exports now face a 20% tariff, while China is hit with 34% (half of the U.S. estimate of China’s total trade barriers) (Trump tariff global reaction – country by country | Trump tariffs | The Guardian) (China readies 34% tariff on US imports starting April 10 | Automotive Dive). India was singled out with a 26% rate, and U.S. tariffs on South Korea were raised to 25% (Trump tariff global reaction – country by country | Trump tariffs | The Guardian) (Trump tariff global reaction – country by country | Trump tariffs | The Guardian). This all-encompassing tariff regime – billed in Washington as “fair reciprocal trade” – stunned markets and provoked swift retaliation threats abroad. China’s Ministry of Finance quickly announced a matching 34% tariff on U.S. goods effective April 10 (China readies 34% tariff on US imports starting April 10 | Automotive Dive), while European officials vowed a united front and prepared countermeasures on up to $28 billion of U.S. imports (Investors seek refuge in dollar, yen as tariff fallout grips markets | Reuters).

Global investors reacted with alarm. Equities were already wobbling late in the prior week as rumors of the tariffs swirled – Japan’s Nikkei 225 slumped ~4% at one point, touching its lowest level in eight months (Trump tariff global reaction – country by country | Trump tariffs | The Guardian), and European stocks drifted lower. When markets reopened on Monday April 7 after the tariffs officially hit, the sell-off intensified into a rout. Wall Street’s S&P 500 plunged ~4.1% on Monday alone, capping a two-session slide that erased more than $5 trillion in market value (Global stock markets tumble further as Trump insists on tariff ‘medicine’) (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters). The chart below shows the S&P 500’s nosedive from late March into early April, as the trade war escalation pummeled U.S. equities:

(File:March 27th to April 7th, 2025, S&P 500.jpg – Wikipedia) Figure: S&P 500 Index, March 27 – April 7, 2025. The benchmark fell sharply from around 5,700 in late March to ~5,100 by April 7 amid the tariff turmoil.

The tech-heavy Nasdaq Composite opened April 7 down over 4% before an intraday rebound – only to sag again by midday (Volatility grips global stock markets as Trump insists on tariff ‘medicine’ | Global economy | The Guardian). Volatility spiked dramatically: the VIX “fear index” hit 60 for the first time since August 2015 during Monday’s chaos (Volatility grips global stock markets as Trump insists on tariff ‘medicine’ | Global economy | The Guardian). In short, the U.S. market entered “bear market” territory, with the S&P 500 flirting with a 20% decline from recent highs (Stock Slide Puts S&P 500’s Bear Market in Sight: Markets Wrap) as investors grappled with the potential economic fallout of a full-fledged trade war.

Asian equity markets were the first to absorb the tariff shock, and they took it on the chin. In Tokyo, the Nikkei 225 index opened sharply lower after the U.S. announcement and at one point was down 4% to an eight-month low (Trump tariff global reaction – country by country | Trump tariffs | The Guardian). By Monday’s close, the Nikkei had entered a bear market of its own – down more than 20% from its peak, the steepest drop among major Asian indexes as of now (Japan’s Nikkei enters bear market – BNN Bloomberg). The surging yen exacerbated the pain for Japan’s export-heavy market, threatening corporate profits for automakers and electronics giants. Japan’s government lobbied furiously for relief: officials in Tokyo called the U.S. tariffs “extremely regrettable” and pressed Washington to exempt Japan, given its status as one of the largest investors in the American economy (Trump tariff global reaction – country by country | Trump tariffs | The Guardian). So far, those pleas have not yielded an exemption, and Japanese automakers are bracing for a hit – Goldman Sachs estimates the new levies will have a “significant” impact on Japan’s auto industry, which sends over 30% of its exports to the U.S. (Trump tariff global reaction – country by country | Trump tariffs | The Guardian).

China’s markets also sagged amid the escalating tit-for-tat. The Shanghai Composite and Hong Kong’s Hang Seng each fell several percent through the week’s end, though Chinese state-backed funds were rumored to be buying shares to stem the decline. Beijing wasted no time in retaliating: on April 4, China’s Finance Ministry confirmed it will levy 34% tariffs on U.S. goods starting April 10, explicitly matching the U.S. duty on Chinese exports (China readies 34% tariff on US imports starting April 10 | Automotive Dive). Additionally, Chinese authorities announced export controls on strategic materials (including certain rare earth metals) and expanded their “Unreliable Entity” blacklist to include more U.S. companies (China readies 34% tariff on US imports starting April 10 | Automotive Dive). These moves signaled that Beijing is willing to retaliate beyond tariffs alone, targeting U.S. supply chains in technology and resources. The prospect of a protracted U.S.-China standoff – with no trade talks even on the horizon (Trump has ruled out negotiations with China for now) (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters) – has darkened the outlook for Asia’s economies. Investors fear a “full-blown trade war” could knock regional export growth into reverse. Accordingly, the Chinese yuan has drifted lower (the offshore RMB is nearing its weakest levels in over a year (Yen Rips, Yuan Dips: The FX Fallout From Trump’s Trade War)), as traders bet that China’s central bank may let the currency soften to buffer the tariff impact (Investors seek refuge in dollar, yen as tariff fallout grips markets).

Elsewhere in Asia, export-dependent markets echoed the downturn. South Korea’s KOSPI slid amid concerns for its electronics and automotive giants. Korea’s government convened an emergency taskforce and vowed an “all-out” effort to support affected industries (Trump tariff global reaction – country by country | Trump tariffs | The Guardian). Notably, Hyundai Motor Co. managed to avoid the worst: the automaker secured a special tariff exemption deal with the U.S. by pledging an enormous investment in American production. In late March, Hyundai announced a $21 billion plan to expand manufacturing in Alabama, build up local supply chains (including steel), and even develop energy infrastructure stateside (Hyundai Agrees To Deal To Avoid Trump’s Tariffs | Global Finance Magazine) (Hyundai Agrees To Deal To Avoid Trump’s Tariffs | Global Finance Magazine). This investment – doubling Hyundai’s historical U.S. footprint – effectively won the company a free pass on the new auto tariffs. “Hyundai will be producing steel in America and making its cars in America, and as a result, they’ll not have to pay any tariffs,” President Trump touted after the deal (Hyundai Agrees To Deal To Avoid Trump’s Tariffs | Global Finance Magazine). Hyundai’s proactive move stands in contrast to Japanese and European automakers, which now face 25% duties on cars they import to the U.S. With Trump threatening to penalize automakers from Canada and Mexico next (25% tariffs on North American-built cars are slated to begin as well), other companies like Honda, Nissan, Volvo, and Volkswagen are reconsidering their supply chains and weighing shifts of production into the U.S. to dodge tariffs (Hyundai Agrees To Deal To Avoid Trump’s Tariffs | Global Finance Magazine). This corporate calculus – essentially “if you can’t beat ’em, join ’em” – highlights how some firms are adapting to the new trade order, even as most of Asia’s business community hopes for the tariffs to be rolled back.

European equity markets were no safe haven in this storm. The pan-European STOXX Europe 600 index fell steadily through the week, shedding about 3% by April 7 and closing around 524 (near its lowest levels of the year). Fears about a hit to Europe’s export machine – especially Germany’s – sent continental indices into the red. In Frankfurt, the DAX index entered correction territory, and in Paris the CAC 40 dropped to a six-month low. Auto and industrial stocks led the decline, unsurprisingly: Europe’s big carmakers like Volkswagen, BMW, and Daimler rely heavily on U.S. sales and now face a 20% tariff on their EU-built vehicles (Trump tariff global reaction – country by country | Trump tariffs | The Guardian). Auto manufacturing CEOs warned that if the tariffs persist, European car exports to the U.S. could plunge by double-digits, putting jobs at risk on both sides of the Atlantic.

Brussels’ response has been firm condemnation – and preparations to retaliate in kind. The European Union has signaled it will present a united front against Trump’s tariffs, resisting any temptation for individual countries to cut side deals. EU leaders met in emergency session and discussed fast-tracking WTO complaints as well as drawing up retaliatory tariffs on iconic U.S. products. According to Reuters, the EU is likely to approve an initial set of counter-tariffs targeting up to $28 billion of U.S. imports, ranging from “dental floss to diamonds” (Investors seek refuge in dollar, yen as tariff fallout grips markets | Reuters). This targeted list seems crafted both to inflict political pressure (hitting goods from key U.S. states) and to minimize harm to European consumers. Still, EU officials stress they prefer a negotiated solution. Germany’s economy minister noted that Europe “will not escalate” if the U.S. reconsiders the blanket approach – but also warned that Europe “will respond one-for-one” if forced. Beyond official channels, there’s talk of Europe deepening trade ties elsewhere (with Asia and South America) to reduce reliance on the U.S. market in the long run.

Despite the volatility, some analysts argue European markets might be comparatively resilient. Goldman Sachs, for instance, trimmed its STOXX 600 target only slightly (to 570 from 580) in light of the tariffs (Goldman Sachs trims Europe’s STOXX 600 forecast on Trump tariff impact | Reuters). The bank noted that Europe’s equity valuations were lower and its investor positioning lighter than the U.S., providing a cushion (Goldman Sachs trims Europe’s STOXX 600 forecast on Trump tariff impact | Reuters). Additionally, expected fiscal stimulus in Europe (e.g. EU-wide infrastructure spending and green investment plans) could help offset some trade-related weakness (Goldman Sachs trims Europe’s STOXX 600 forecast on Trump tariff impact | Reuters). This means European stocks might rebound faster if clarity on trade emerges. Indeed, on Monday the FTSE 100 in London fell only modestly (-0.5%), outperforming other regions – thanks in part to a weaker British pound (which hit a one-month low around $1.28, boosting UK multinationals’ overseas earnings) (Investors seek refuge in dollar, yen as tariff fallout grips markets | Reuters) (Investors seek refuge in dollar, yen as tariff fallout grips markets | Reuters). Similarly, Switzerland’s SMI index was relatively steady, as investors fleeing risk pushed the Swiss franc so high that it may prompt the Swiss central bank to intervene to cap the currency (Investors seek refuge in dollar, yen as tariff fallout grips markets | Reuters). In summary, Europe is bruised by the U.S. tariffs, but it’s responding with a mix of resolve (unified countermeasures) and relief that it maintains some structural advantages (valuation and current-account surplus) to weather the storm (Investors seek refuge in dollar, yen as tariff fallout grips markets | Reuters).

Within the U.S. stock market, the pain was widespread but tech and consumer giants were hit especially hard. The famed “Magnificent Seven” – Apple, Microsoft, Alphabet (Google), Amazon, Tesla, Meta (Facebook), and Nvidia – saw their collective market cap shrink by roughly $2 trillion on Monday as the sell-off intensified (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters) (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters). These seven stocks, which had led the market’s gains in recent years, have now lost over $6 trillion in value since their peak in late 2024 (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters). Apple, an emblematic case, dropped 4.8% on April 7 to a one-year low (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters). Analysts warn that Apple faces a “complete disaster” from the new tariffs since most iPhones are assembled in China – meaning the 34% U.S. import tax could either force huge price increases or crush Apple’s margins (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters) (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters). (Apple had secured exemptions to tariffs during Trump’s first term, but it’s unclear if the company can win waivers this time despite recently announcing a $500 billion U.S. investment plan (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters).) Likewise, Tesla shares plunged 7% (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters) as experts noted the company’s dual vulnerability: higher costs on Chinese-made components and a potential consumer backlash in China. Elon Musk’s vocal support of Trump’s policies has turned off Chinese buyers, and rivals like BYD stand ready to capture any opening (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters). A Wedbush analyst slashed price targets for both Apple and Tesla, warning of a “tariff economic armageddon” scenario for U.S. tech unless tensions ease (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters).

Other sectors mirrored the carnage. U.S. automakers and industrials fell sharply on fears of retaliatory damage to overseas sales. Agricultural firms and commodity producers dropped as China (a huge buyer of U.S. soybeans, pork, and airplanes) signaled it would not back down. In fact, China’s 34% tariff directly strikes U.S. farm goods, aerospace, and electronics exports (China readies 34% tariff on US imports starting April 10 | Automotive Dive), sending those sector stocks tumbling. Bank stocks struggled as well, with recession odds rising and yield curves flattening. Goldman Sachs boosted its estimated probability of a U.S. recession in the next year to 35% (from 20% prior) on the tariff news (Goldman Sachs trims Europe’s STOXX 600 forecast on Trump tariff impact | Reuters), and JPMorgan’s CEO Jamie Dimon cautioned that the tariffs “will likely increase inflation and slow down growth” if they persist (Volatility grips global stock markets as Trump insists on tariff ‘medicine’ | Global economy | The Guardian). Notably, some high-profile Trump supporters in the business community have broken ranks in recent days. Billionaire investor Bill Ackman (who had backed Trump’s campaign) blasted the tariff strategy, saying “we are heading for a self-induced, economic nuclear winter” and urging the administration to reconsider (Volatility grips global stock markets as Trump insists on tariff ‘medicine’ | Global economy | The Guardian). Such stark language from typically bullish voices underscores the level of concern pervading Wall Street.

On a slightly positive note, energy stocks and other cyclicals found a silver lining as oil prices initially rallied earlier in the week on hopes that OPEC+ might cut output to support the market. However, by Monday even crude oil succumbed to demand fears: Brent and WTI oil benchmarks plunged ~3% on April 7 to their lowest levels since 2021 (COMMODITIES Oil drops to four-year low, metals fall on recession fears | Reuters) (COMMODITIES Oil drops to four-year low, metals fall on recession fears | Reuters). Over the past week, oil has shed more than 10% of its value (COMMODITIES Oil drops to four-year low, metals fall on recession fears | Reuters), which actually provides a bit of relief to consumers and transport companies (lower fuel costs) even as it signals economic stress. Gold miners and metal producers also sold off, with copper and nickel prices hitting multi-year lows amid expectations that a global slowdown would sap industrial demand (Miners Drop to Multiyear Lows as Tariff Turmoil Rocks Metals). In short, virtually every corner of the equity market – save for defensive plays like utilities and certain healthcare names – has been touched by the tariff turmoil.

As we enter the second week of April, investors are asking: Has the market priced in the worst, or could the sell-off deepen? Much will depend on how the trade conflict evolves in the coming days. China’s retaliatory tariffs are scheduled to take effect on April 10 (China readies 34% tariff on US imports starting April 10 | Automotive Dive), and traders will be watching closely for any last-minute negotiations or surprises. So far, both Washington and Beijing appear entrenched – Trump doubled down over the weekend, insisting tariffs are the necessary “medicine” for unfair trade and even telling Americans to “endure the pain” for now, while ruling out talks with China (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters). If this hard line persists, markets may remain volatile or grind lower as the economic impacts start to materialize. By mid-week, companies will begin reporting Q1 earnings, and forward guidance from multinationals will be scrutinized for hints of tariff-related weakness. Any high-profile profit warnings could trigger further sell-offs.

On the other hand, policymakers are also likely to respond. Central banks have already turned more dovish – the question is how much more they’ll do if conditions worsen. The Fed, which had been on pause, could signal rate cuts or other support if U.S. financial conditions tighten further (Goldman now expects three Fed rate cuts this year, up from two, given the tariff shock (Goldman Sachs trims Europe’s STOXX 600 forecast on Trump tariff impact | Reuters)). Similarly, the European Central Bank may accelerate easing plans if the Eurozone economy falters under trade pressures (Goldman Sachs trims Europe’s STOXX 600 forecast on Trump tariff impact | Reuters). Such monetary stimulus prospects could help put a floor under asset prices, as they often have in past sell-offs. Moreover, there is the chance of political recalibration: mounting outcry from businesses and consumers might push the U.S. administration toward the bargaining table. Indeed, market free-fall can become self-correcting if it prompts policy moderation. For example, if U.S. equities approach a bear market and key stakeholders complain loudly, the White House could soften its stance or carve out more exemptions (as it did for Hyundai and potentially for select U.S. companies like Apple (Tariff storm ravages Magnificent Seven as Apple nears one-year low | Reuters)).

In Europe, the coming week may bring a formal announcement of the EU’s counter-tariffs. While largely symbolic in near-term economic terms (the mooted $28 billion of U.S. goods is relatively small), such a move would cement the “everyone against one” trade rift, potentially dampening sentiment further. Still, any sign of diplomacy – even back-channel talks or a temporary halt on new tariffs – would likely spark a relief rally given how pessimistic expectations have become. With volatility elevated and correlations high, investors should brace for more seesaw action. Safe-haven assets like the yen, franc, Treasurys, and gold will be key barometers of risk appetite: if we see those retrace some gains, it may indicate stabilization. Conversely, new highs in those havens would spell continued defensive positioning.

Bottom line: the global equity rout from April 4–7, 2025 has been a stark reminder of how sensitive markets are to trade policy. Major indices are flashing oversold signals, but the catalyst for a rebound is not yet evident. Absent clarity on the U.S.-China-Europe trade showdown, the path of least resistance might still be choppy or downward for equities. Investors should keep an eye on political developments – a tweet, a meeting, or a tariff tweak can swiftly alter the narrative – as well as on economic data that reveal how much damage is (or isn’t) being done. In the meantime, caution reigns. The coming week will test whether this tariff storm is a temporary squall or the start of a longer bear market voyage for global stocks.

{kind=link}